Machine Learning is Just One Part of the Solution

You could say that fraud and eCommerce security have a very roundabout, symbiotic relationship.

As security tools and strategies improve, so do the schemes fraudsters employ to get around those roadblocks. In turn, these new threat sources create the need for new, more intelligent, and more dynamic responses. Unfortunately, this also means devoting more and more resources to prevent fraud rather than toward productive goals like acquiring new customers or improving the shopping experience.

There is a tool, however, that may dramatically change our approach to identifying and mitigating fraud: machine learning.

First Things First: What is Machine Learning?

Machine learning has been a hot topic in security and payments circles for a few years. If you’re not familiar with the concept, machine learning is just as it sounds: studying and advancing the way computers “learn.”

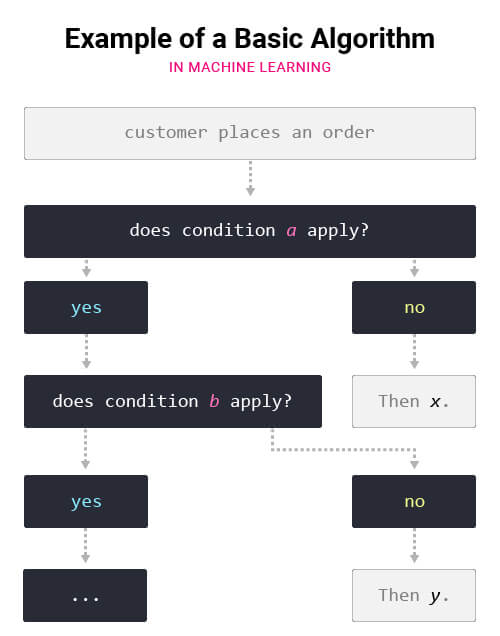

The computers are not “learning” in the way that a person or animal would; the arrival of genuine artificial intelligence is still many years away. Instead, machine learning assembles and adds to a complex web of algorithms that, over time, enable computers to make more nuanced, complex decisions. For example, look at the basic algorithm in the chart below:

While this is very simplified, the basic idea is the same. Algorithms are how computers “think,” and machine learning describes the addition of new algorithms as computer “knowledge.” This builds an increasingly complex system of rules that will determine the computer’s decisions over time.

How Machine Learning Make Fraud Prevention Simple

Machine learning idea has incredible implications for fraud prevention. The algorithms that make up the process are compiled from real-world historical data based on identified threats and fraud attacks. The computer is then able to draw a more accurate impression of whether a transaction is fraudulent.

Machine learning allows fraud and loss prevention professionals to operate strategically. Rather than choosing between manual review of each individual transaction and firing into the dark, machine learning produces better and more accurate automated processes. More fraudulent transactions are intercepted, and false positives decrease as the machine’s intelligence increases.

With the benefit of machine learning, retailers reduce the time and money devoted to manual review. A small team with intelligent computer processes can handle what otherwise would have called for an entire office of people just a few years ago.

Remember: No Technology is Perfect.

That said, don’t make the mistake of being over-reliant on machine learning. No automated process, no matter how intelligent, will ever be flawless.

The fact that machine learning relies on historical data is just as much a weakness as it is an asset. New threats appear every day. Fraudsters develop attack plans and strategies to separate merchants from their money faster than machines can identify and respond to them.

The rate at which fraud evolves means data on the subject can never really be complete. Therefore, basing your entire fraud defense on analysis of historical data limits your ability to be proactive in fighting back and protecting the business. You may be able to intercept fraud attacks that are based on previously-identified threats and logical successive techniques, but machine learning on its own can only do so much.

Look at chargebacks, for example. We know that there are three primary sources of chargebacks:

- Criminal Fraud

- Friendly Fraud

- Merchant Error

Machine learning can identify the signs associated with criminal fraud, and can help pinpoint the policy and practice oversights that lead to merchant error chargebacks. However, computers can’t predict friendly fraud attacks because they are seemingly legitimate transactions. The fraud doesn’t come until well-after the transaction is complete.

The Answer: Machine Learning & Human Oversight

It’s true: machine learning has great potential for fraud prevention, but is also highly susceptible to miss newly-developed fraud attacks or loss sources that come post-transaction. That’s why it’s important that you adopt machine learning technologies as just one element of an effective fraud mitigation strategy.

The most important element is the human element. Humans oversight is a vital component in a dynamic approach to fraud. While computers can apply complex algorithmic logic much faster and more efficiently, humans are able to think in a more dynamic, multi-dimensional manner. For example, compare live customer service to chatbots. While chatbots can be a great first-line strategy to offer quick and responsive service, there are certain things they simply can’t do:

- Chatbots max-out at about 85% efficiency in customer service capacities.

- They can’t interpret intent or the meaning of words as well as humans.

- They can’t think abstractly to identify and resolve more complex problems.

Machine learning and human expertise complement one another, and are equally important to create an effective fraud response.